We Scraped 84,665 ChatGPT Ad Cards: What the "New Shelf" Inside AI Answers Looks Like (GEOly AI Data Report)

Hi, I’m Riven.

This piece is a little different: the data all comes from our own product, GEOly AI, and its live monitoring system. From late May to mid-June 2026 we watched the ads appearing inside ChatGPT answer pages for nearly a month and captured 84,665 ad cards. Today I’m laying that first-party dataset out for you — what the “new shelf” inside AI answers actually looks like, who’s already in, and what you should do.

Bottom line: the “second battlefield” of search advertising is open

For years, your ad battlefields were Google and Amazon. Now there’s a new one — the ChatGPT answer area.

When a user signals buying intent in a conversation (“recommend a few e-bikes good for commuting”), ChatGPT will insert product ad cards right into the answer — with image, title, selling points and a buy link. And crucially: these paid cards appear in the same frame as the brands the model recommends “organically.” That’s exactly why I keep saying — in the AI era, paid advertising (SEM) and GEO (Generative Engine Optimization) have to be done together. They’re fighting for position on the same answer page.

Every claim below is based on GEOly AI’s captured sample. Let me put the sample size on the table first, so no one says I’m guessing:

| Monitoring scope | Value |

|---|---|

| Platform | ChatGPT (100% of sample) |

| Window | 2026-05-23 → 2026-06-19 (~4 weeks) |

| Ad cards captured | 84,665 |

| Advertisers covered | 2,352 |

| Topics triggering ads | 12,574 |

Note: this is “what users actually see,” not OpenAI’s back-end data — which makes it the closest read on the real exposure format.

Insight 1: In mid-June, ChatGPT ads surged 8.5x in a single week 🚀

This is the single most important signal in the dataset. By week, ad-card volume:

| Week (start) | Ad cards | Active advertisers |

|---|---|---|

| 05-25 | 4,922 | 489 |

| 06-01 | 7,073 | 757 |

| 06-08 | 7,639 | 795 |

| 06-15 | 65,010 | 1,659 |

In the week of June 15, card volume jumped from 7,639 to 65,010 — about 8.5x week-over-week; advertisers doubled (795 → 1,659) in a week.

This obviously isn’t organic growth — it’s OpenAI opening the inventory floodgates. What does it mean for sellers? Inventory exploded, bid pressure hasn’t caught up = click costs are sitting in a trough right now. Once everyone wakes up and prices grind upward, the window closes. This is the textbook channel-launch phase.

Insight 2: Almost everyone in is US retail/DTC — Chinese cross-border sellers are absent

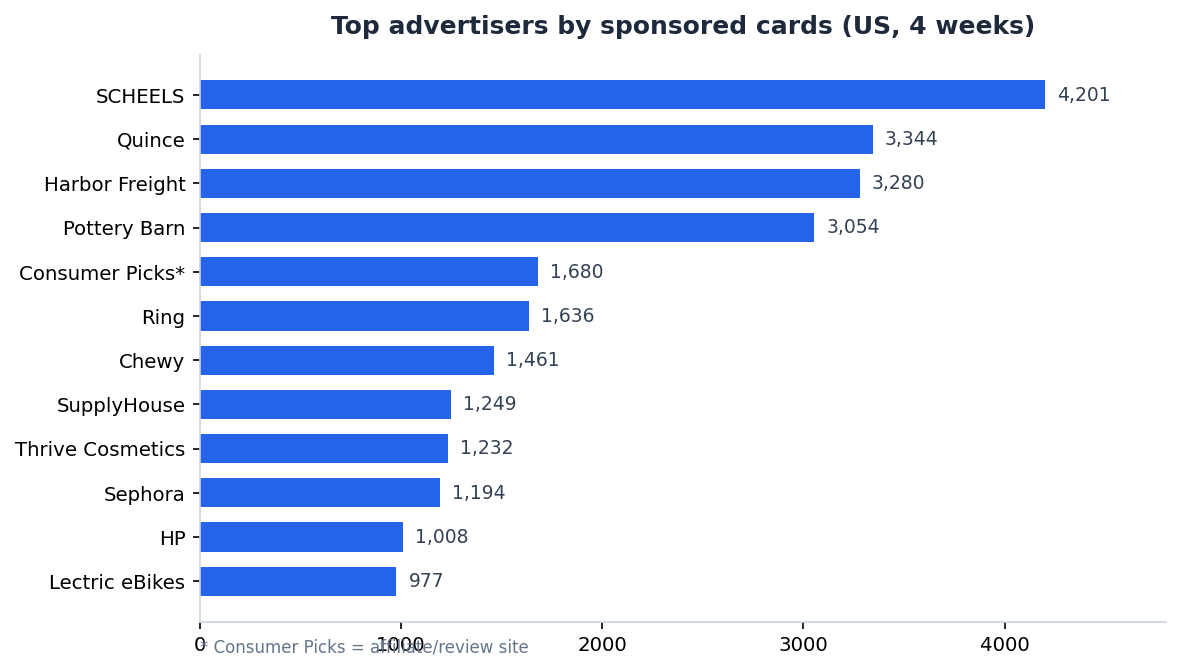

Ranked by card volume, the top advertisers look like this (Top 15):

| Advertiser | Cards | Topics |

|---|---|---|

| SCHEELS | 4,201 | 2,226 |

| Quince | 3,344 | 1,302 |

| Harbor Freight | 3,280 | 1,220 |

| Pottery Barn | 3,054 | 1,383 |

| Consumer Picks | 1,680 | 706 |

| Ring | 1,636 | 540 |

| Chewy | 1,461 | 503 |

| SupplyHouse | 1,249 | 663 |

| Thrive Causemetics | 1,232 | 524 |

| Sephora | 1,194 | 631 |

| HP / Lectric eBikes / Home Depot / Zenni / e.l.f. | … | … |

Top advertisers ranked by sponsored cards — SCHEELS, Quince, Harbor Freight and Pottery Barn lead (GEOly monitoring, US, 4 weeks)

Top advertisers ranked by sponsored cards — SCHEELS, Quince, Harbor Freight and Pottery Barn lead (GEOly monitoring, US, 4 weeks)

Concentration: Top 10 advertisers hold 26.4% of cards, Top 50 hold 50.9% — but the tail is very long (2,352 advertisers).

See the problem? They’re all US retailers and DTC brands (department stores, home, hardware, beauty, pet, eyewear, e-bikes). I combed the top ranks and could barely find a single Chinese cross-border seller.

That’s an opportunity gap for you: competitors haven’t come in to educate the market yet — whoever builds “shelf presence inside AI answers” first locks in position at the lowest cost.

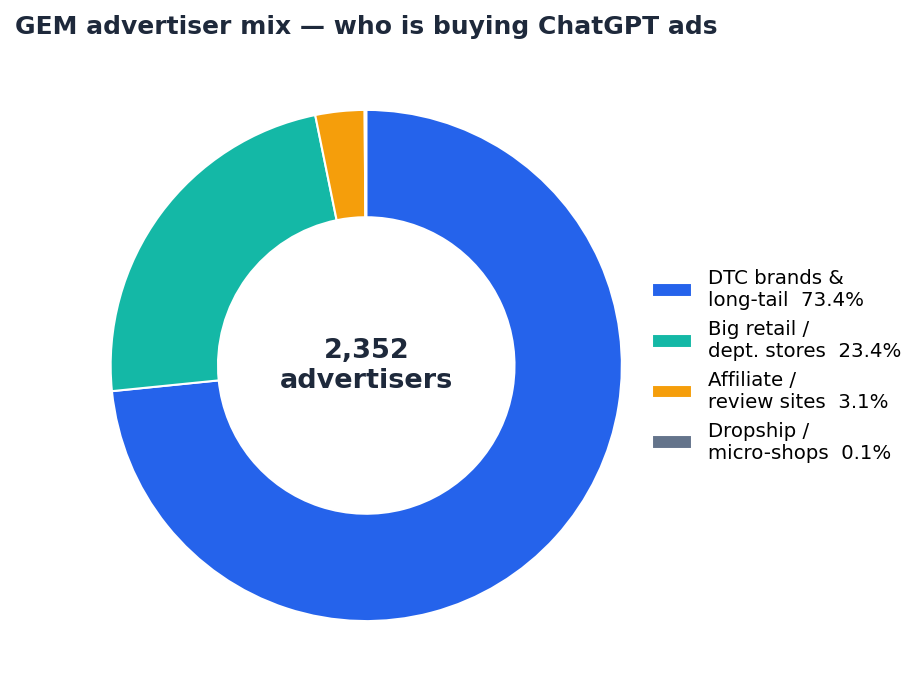

What types of advertisers are there?

Group the 2,352 advertisers by “monetization model x shelf position” and it gets clearer:

By card volume, advertisers fall into four types (GEOly data)

By card volume, advertisers fall into four types (GEOly data)

- ① DTC brand-owned sites (the bulk, ~73%): Quince, Thrive, Zenni, Lectric eBikes, e.l.f., Ring… 88% of ads route traffic back to their own site — essentially the challenger’s weapon to bypass the giants’ organic monopoly.

- ② Big retail / department stores (18 leaders = 23%): SCHEELS, Pottery Barn, Home Depot, Macy’s, Sephora — few players, massive coverage.

- ③ Affiliate / review / ranking sites (~3%): the likes of Consumer Picks — no products of their own, monetizing via referral.

- ④ Resellers / dropship micro-shops (~0.1%): barely advertise at all — they occupy “organic shelf cards,” not paid cards.

A counterintuitive point: the pure marketplace giants (Amazon / Walmart / Target) are largely absent from paid ads, while category retailers are already heavily in — leaving mid-size brands a window to stand on the same stage as the giants.

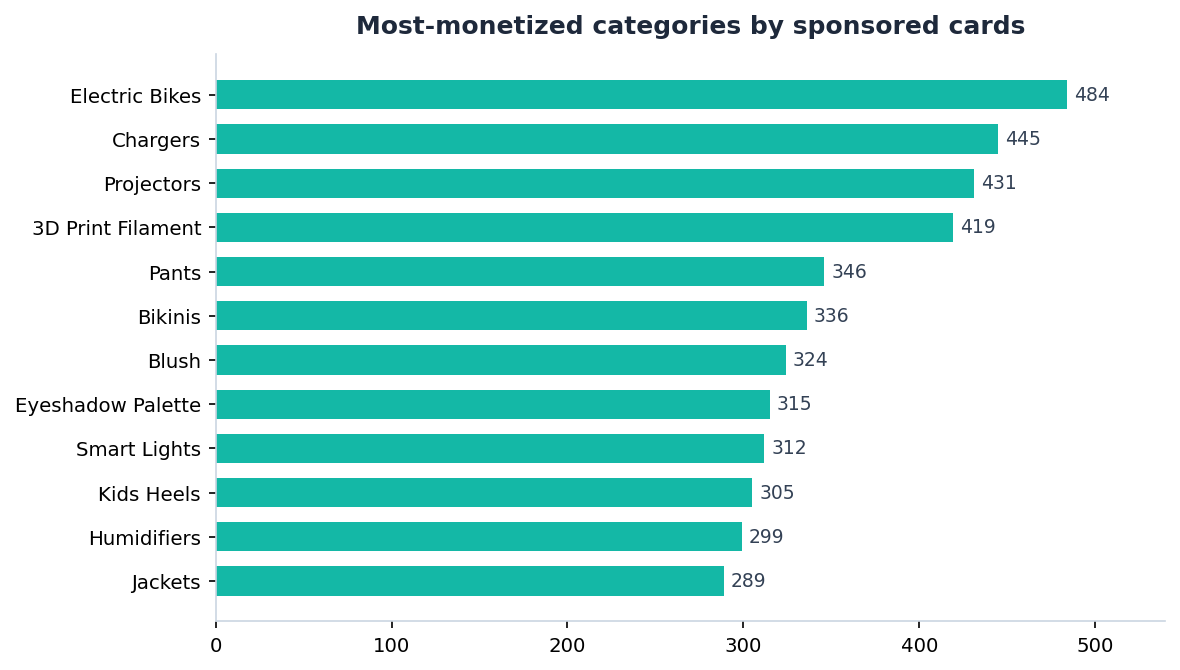

Insight 3: The more “research-heavy, high-ticket” the category, the more likely it triggers ads

Among the high-frequency triggering topics GEOly captured, e-bikes nearly own the leaderboard: fast electric bikes, folding electric bikes, electric bikes for commuting, mini electric bikes…

What’s more interesting is the number of bidders on these topics — many have just 2–6 advertisers fighting. In other words, there’s a huge supply of “high purchase intent x low competition” long-tail pockets. For new entrants, that’s exactly the gap to cut into.

By sponsored cards, e-bikes, chargers, projectors, 3D-printing filament, beauty and apparel run hottest (GEOly monitoring)

By sponsored cards, e-bikes, chargers, projectors, 3D-printing filament, beauty and apparel run hottest (GEOly monitoring)

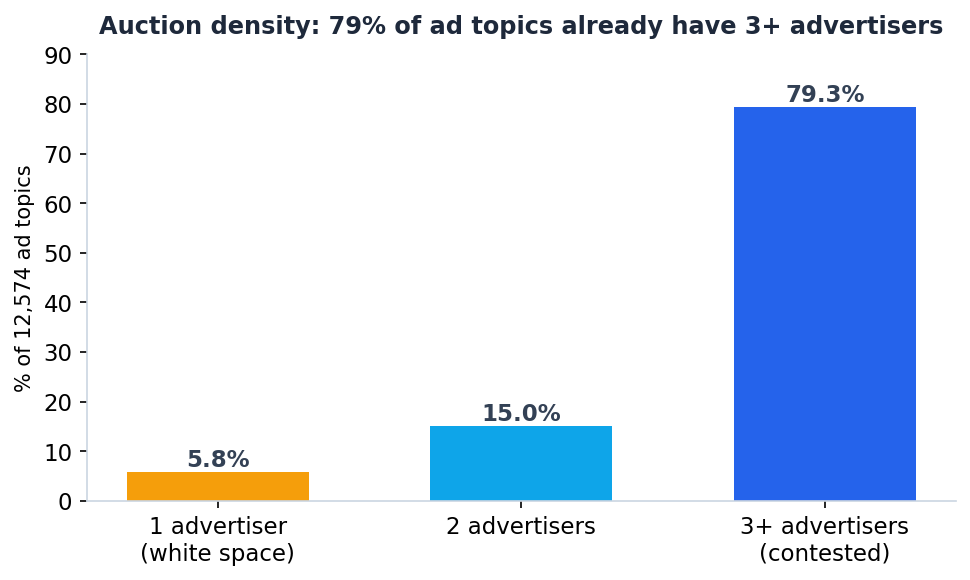

But here’s the cold water: overall competition is already getting crowded. Across the full library, the average topic has 4 advertisers bidding, and 79% of topics already have 3+ advertisers on the stage:

Only 5.8% of topics are still single-advertiser “white space” (GEOly monitoring)

Only 5.8% of topics are still single-advertiser “white space” (GEOly monitoring)

So a “pocket” doesn’t mean “no one’s bidding” — it means “amid the general shift to red oceans, there are still ≤2-advertiser half-empty slots.” Pick keywords on both demand and crowding — avoid the hot, grab the empty.

Insight 4: Ads = SKU-level shopping cards, not brand banners

By creative content, ChatGPT ads are basically product-level shopping cards (title = a specific product, body = scenario-driven selling points), not brand image ads. For example, cards captured from Chewy (pet ecommerce):

CarSafe Crash Tested Back Clip Dog Harness, Blue, Large— “Remember to measure your pet for the paw-fect fit…”Automatic Cat Feeder— “Make mealtime easier.”

The pattern is clear: the title is a buyable product, the copy is conversational, scenario-fit selling points, and the landing page goes straight to the PDP. It rewards “structured product data + scenario copy” — the same underlying craft as GEO content optimization. Your product feed quality directly decides whether you get picked for display.

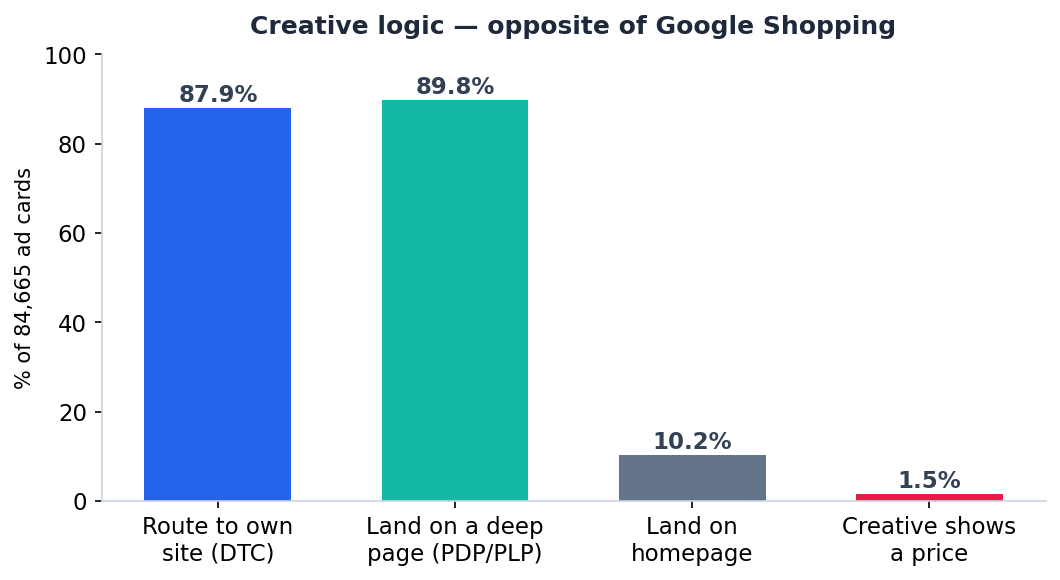

88% route to their own site, 90% land on a deep buyable page, only 1.5% of creatives show a price (GEOly data) — GEM doesn’t run price wars; it builds “category shelf entries”

88% route to their own site, 90% land on a deep buyable page, only 1.5% of creatives show a price (GEOly data) — GEM doesn’t run price wars; it builds “category shelf entries”

Three real cases, three playbooks

① Lectric eBikes — narrow-niche depth, density domination. 977 cards across just 166 topics — a per-topic density of 5.9 cards (one of the highest). It doesn’t spread wide; it locks long-tail keywords inside the single e-bike vertical, where bidders number only 2–6. This is the most replicable playbook for SMBs: concentrate budget and dominate one category.

② Consumer Picks — review-ranking interception. It pushed into the Top 5 with 1,680 cards, all creatives like Top 10 Dash Cams 2026 — Reviewed and ranked by experts. There's one clear winner., landing on its own review site. It doesn’t sell products; it sells the “third-party ranking trust slot,” then routes traffic to monetize. A warning: the category you pay to educate may be getting its clicks skimmed by a ranking site at lower cost.

③ Chewy — dual-granularity coverage. It runs both precise SKU cards (high conversion) and broad category cards Large Cat Trees → "Shop cat furniture at Chewy." (mindshare). Mature players play both hands.

5 action items for cross-border sellers

- Get in and test now. The mid-June inventory surge is a bid trough — use 5–10% of budget to grab cheap early share; don’t wait for maturity.

- Pick pocket topics. Prioritize “high-intent x ≤5 bidders” long-tail keywords; avoid red oceans like e-bikes and accessories.

- Cover at dual granularity. Combine precise SKU cards with broad category cards; don’t bet on just one.

- Treat your feed as creative. Rewrite product titles, selling points, images and prices for the “conversation scenario” — structured data quality decides your selection rate.

- Run ads and GEO together. Ads alone get diluted by organic recommendations; GEO alone misses the paid fast lane — they only work as one play on the same answer page.

A closing note — on this dataset, and GEOly AI

Every number in this piece comes from GEOly AI’s continuous monitoring of ChatGPT answer pages — tracking ad cards’ appearance, share and creatives platform-by-platform, topic-by-topic, advertiser-by-advertiser, while also tracking brands’ organic mentions in AI answers. Put simply, it’s our “telescope” for seeing this new battlefield clearly.

In the Google era we learned SEO + SEM. In the AI-answer era, GEO + AI advertising is the new default. This ChatGPT ads window is opening earlier — and will close faster — than you think.

Want to see your own category’s ads and mentions inside ChatGPT? Run a diagnosis at GEOly AI. We’ll keep publishing this monitoring data — follow Riven, follow GEOly AI, and let’s take this new shelf inside AI answers together.

Related: How Do You Actually Run ChatGPT Ads? The “Two Shelves” Playbook

— Riven & the GEOly AI team

Data note: sample is GEOly AI public monitoring data (2026-05-23 to 2026-06-19, 84,665 ChatGPT ad cards), reflecting user-visible ad presentation, not OpenAI’s official placement data. Bid/cost-related conclusions are inferences based on exposure patterns.